Bitcoin Rallies Higher Even As Derivatives Lack Conviction

Key takeaways:

- While Bitcoin onchain activity and derivatives show a lack of participation from traders, record spot ETF inflows point to strong institutional demand.

- The absence of leveraged longs may actually fuel further upside as sellers are forced to buy back if Bitcoin edges higher.

Bitcoin (BTC) gained 7% over the past week, breaking above $81,000 for the first time in over three months. Despite the strong price performance, data suggest that Bitcoin derivatives lack optimism from investors and this raises questions on the rally’s sustainability.

Bitcoin derivatives fail to mirror investors’ joy over $81,000

Macroeconomic and several onchain metrics point to softening demand.

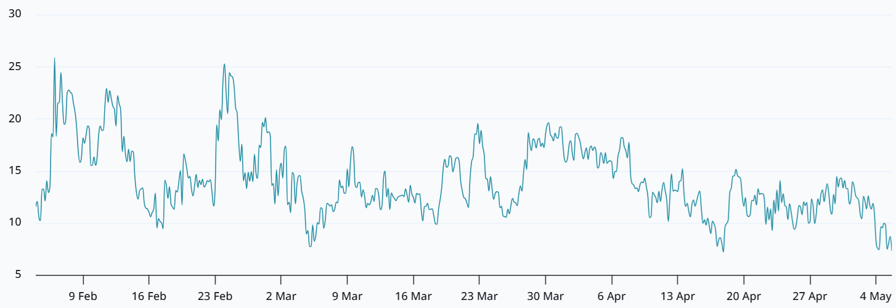

Bitcoin 2-month futures basis rate. Source: Laevitas

Bitcoin monthly futures traded at a 1% annualized premium (basis rate) relative to spot markets on Tuesday, landing well below the neutral threshold. Typically, sellers demand a 4% to 8% premium to compensate for the cost of capital. This cautious sentiment took hold in late January, when Bitcoin was trading at $90,000, partly explaining the current lack of enthusiasm.

To confirm if the issue is limited to futures, one should assess the demand balance between put (sell) and call (buy) options. Under neutral conditions, these instruments trade within a -6% to +6% premium relative to each other. When professional traders fear downside risks, the delta skew metric moves above 6%.

Bitcoin 30-day options delta skew (put-call) at Deribit. Source: Laevitas

The Bitcoin delta skew moved closer to the 6% neutral threshold on Tuesday, though it remained slightly bearish. Whales and market makers do not appear particularly worried about an imminent crash, but bulls’ conviction has clearly stagnated. With Brent crude oil prices hovering near $110, persistent inflation concerns are weighing on traders’ expectations for economic growth.

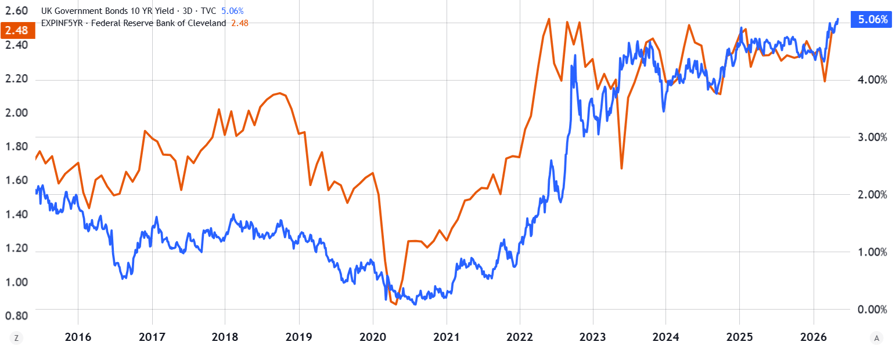

US 5-year inflation expectation vs. Euro 10-year government bond yields. Source: TradingView

US inflation expectations neared a 10-year high of 2.5%, according to data from the Federal Reserve Bank of Cleveland. Simultaneously, investors are demanding higher returns to hold Eurozone government bonds. Despite these inflationary pressures, the tech-heavy Nasdaq 100 Index surged to an all-time high on Tuesday, signaling a broader risk-on environment.

Declining Bitcoin onchain activity faces heavy spot ETF accumulation

Bitcoin may have benefited from this increased risk appetite, but weak onchain metrics hints with declining retail demand.

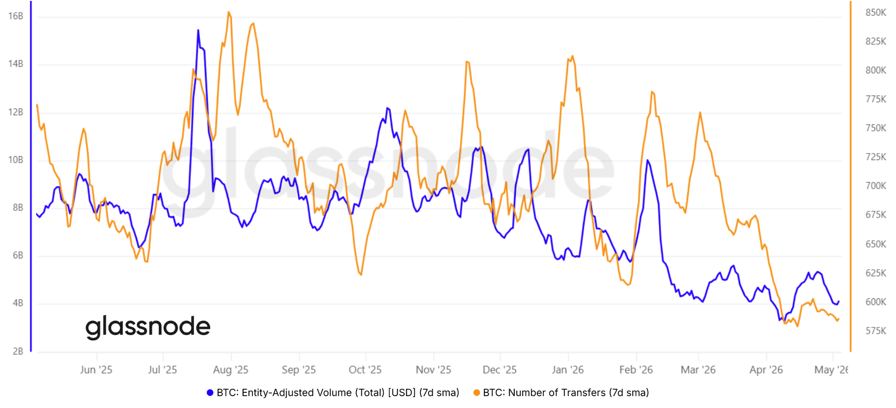

Bitcoin onchain daily volume (USD) vs. number of transfers. Source: Glassnode / Cointelegraph

Daily network transfer volume has plummeted 54% from three months ago, dropping to $4.1 billion. Similarly, the number of transfers is nearing its lowest level in over five years. While Bitcoin’s price action is not strictly dependent on onchain activity, these metrics serve as a proxy for general public interest and adoption.

The temporary pause in Strategy’s (MSTR US) accumulation ahead of its earnings release may have sparked some unwarranted fear. The company, led by Michael Saylor, maintained an aggressive acquisition pace over the previous four weeks. However, analysts expect Strategy to report a quarterly net loss due to its mark-to-market Bitcoin accounting.

Related: Bitcoin turns risk on as stocks hit new highs and miner profits rise: Is $85K BTC next?

Macroeconomic weakness and declining onchain activity negatively impacted Bitcoin derivatives, but the $1.16 billion in net inflows into US-listed Bitcoin spot exchange-traded funds (ETFs) between Friday and Monday suggests rising institutional demand.

Ultimately, the lack of demand for leveraged bullish positions in Bitcoin derivatives might serve as a catalyst for further upside. As prices climb, shorts (sellers) may be forced to close their positions at a loss, fueling additional momentum.